result

result

PREVIOUS

NEXT

Follow Us

All content Copyright 2024 Fixed Income Insights. All rights reserved.

Municipal Markets

BY Abigail Urtz, FHN Financial

Tax-Exempt Bonds Still On the Chopping Block

The debate over the fate of the tax-exemption is still raging in Washington. Industry advocates have been busy defending the exemption as a critical financing mechanism to support US infrastructure, and while advocacy efforts appear to be gaining supporters in some powerful committees, the threat of losing the exemption is still real. A House budget outline circulating through DC includes massive promises on tax and spending cuts that still need pay-for’s in the trillions of dollars, meaning everything is “on the table,” including tax-exempt benefits for issuers and bondholders.

Although Senate leaders are taking a substantially slimmed down approach to the spending bill that could save subsidies like the tax exemption generally viewed to have bipartisan support, other comments in recent weeks have raised concerns that municipal bond subsidies may not be as immutable as once thought. Regardless of how it shakes out, the road to passage of any budget bill is likely to be a long and bumpy one, so market participants should brace for further volatility in bond valuations at least through the spring.

As lawmakers dive deeper into the menu of pay-for’s to fund an extension of the 2017 tax cuts, we see two approaches to the tax exemption starting to take shape, both with considerable impacts on the municipal market.

A Full Repeal of the Tax-Exemption, Applied Prospectively

For now, we believe any attempt to eliminate the exemption on municipal bonds is unlikely to target outstanding securities, while odds of prospective new issues losing their benefit are closer to a coin flip. Private activity bonds and those supporting certain not-for-profit institutions such as private universities and even hospitals face higher odds of losing their exemption. We’ll tag those odds at upwards of 70%, likely with some carveouts such as affordable housing. Here, we consider a full repeal of the tax-exemption and its impacts.

If new bonds were to lose their exemption in full, we would expect spreads on outstanding tax-exempts to tighten considerably on a scarcity trade, likely to the low 60%/high 50% handle relative to 10yr Treasuries. While the bid for these bonds would strengthen significantly, their availability in the secondary market would become extremely limited as they would almost certainly become the asset of last resort to liquidate.1 New bonds would come in taxable form, which would reshape the market in a number of ways.

On the issuer side, financing costs would go up, which would mean higher taxes, less spending, or some combination of both. We also worry issuers would scale back capital projects during the transition phase (three years)2 to avoid hitting residents with higher taxes and fewer services, which have already been slashed by DOGE. The timing is tough given still-high inflation, elevated interest rates, and extensive capital needs for deferred maintenance and climate resilience, not to mention a now-slowing economy that will further crimp revenues. It’s reasonable to think of impacts in economic terms as any “kick the can” behavior will translate to higher costs down the road. As just one example, it’s estimated that a dollar spent today on climate resilience will save 6-13 dollars on recovery costs in the future. The costs of inaction could add up.

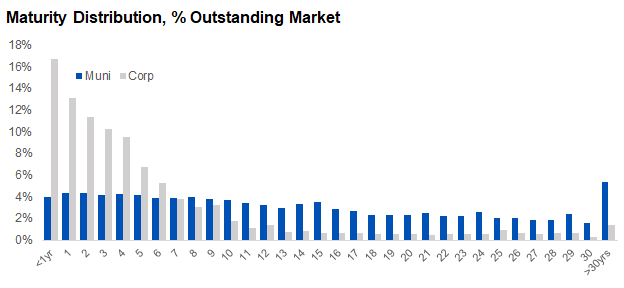

Importantly, only larger, more liquid issuers would have consistent access to the public debt markets as a taxable asset class. The municipal market is notoriously home to thousands of small issuers that infrequently issue debt and/or utilize more “off the run” credit structures. Without retail odd lot buyers to support this market, these smaller issuers may be forced to consider alternative and more costly financing methods to raise capital. As we’ve highlighted previously, these changes, in combination with new onerous reporting requirements under the FDTA, are likely to result in the proliferation of bond banks to pool risk into larger, more liquid issues. There would likely be other structural tweaks to amortization schedules, call options, and couponing to more closely mimic the corporate bond market.

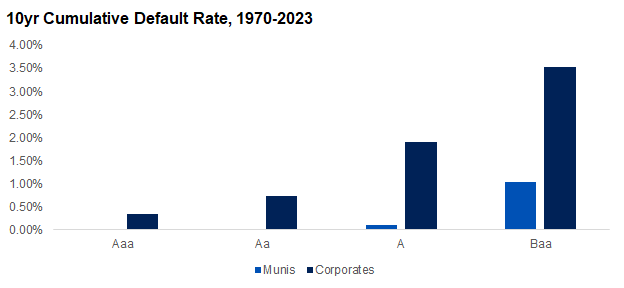

On the investor side, a taxable muni market would have transformative effects. Retail investors would likely significantly curtail purchases, shifting participation to banks, insurance companies, pension funds, and even foreign investors that see less benefit in shielding income from taxes. Municipal issuers have traditionally matched bond maturities to the useful life of capital projects, meaning maturities have been more heavily weighted to the long end than in the corporate space. This could make for a steeper yield curve and attractive relative values vis a vis corporates in longer maturities. In general, we see taxable municipal spreads eventually tracking those of comparably rated corporates. However, spreads are likely to be wider than corporates of like ratings in the transition period as the market works to build an investor base. This could present attractive buying opportunities across the curve, especially given the much lower credit risk in municipals.

Source: Bloomberg

Source: Moody’s

A 28% Cap on the Tax Benefit (Unclear on Potential Application to Outstanding Munis)

Over the past month, we’ve also contended with the reintroduction of perhaps an even more problematic approach to municipal subsidies, which is a 28% cap on the tax benefit. For anyone residing in a higher tax bracket, this would effectively create a tax on municipal interest payments equal to the difference between an investor’s tax bracket and 28%. Given that most tax-exempt municipal bond income is earned by investors residing in very high brackets, this could have substantial impacts on municipal valuations, with nominal yields likely to push 15% higher in equilibrium to find enough buyers.

Source: IRS

If the cap were applied across the board to outstanding and new issue munis alike, impacts on investor portfolios would be ugly. With liquidity in the market already strained by the departure of many institutional investors and dealer sponsors, we would expect a significant selloff pushing yields more than 15% higher and producing losses of 5pts or more in intermediate defensive coupons. Some would argue March’s selloff in municipals is already reflecting some of this move so we may be part of the way there.

Source: MMD, FHN Financial

Note: The 2011 headline reflects a 9/13/11 report on Obama’s Jobs Act proposal. Although the first public headline about the 28% cap in 2025 came with the Stephen Moore report on 3/21/25 (day 10), there were prominent whispers about the proposal starting on March 7

To demonstrate the impact, let’s consider an investor in the highest tax bracket of 40.8%. For this buyer, a 3.5% nominal yield in the municipal market today would equate to a taxable equivalent yield of 5.91%. If this investor faced a cap on the benefit of 28%, their taxable equivalent yield would fall by over 100bp, to 4.86%. To achieve the same taxable equivalent yield they received before, this investor would have to demand a nominal yield of 4.25, 75bp (21%) higher than the pre-cap yield. For anyone counting, that’s a nearly 7pt loss on a 10yr 5% coupon bond. Even if we incorporate the lesser yield demands from investors in lower tax brackets, we come out to a weighted average demand for nominal yields that are 15% higher than they are today.3

Of course, this represents where the market could settle. In reality, the initial impact could be much greater. We estimate an initial spike in intermediate rates of closer to 20-25%, which would carry a price impact of 6-8pts.

While hard to quantify, perhaps the most long-term damage could be caused by the change in investor psyche if what has long been considered sacrosanct - tax-free income - becomes taxable and results in substantial losses in municipal values overnight. Regardless of where the cap is set, once the door is opened, investor trust will be broken and participants will have to price in the risk of further reductions in the cap going forward.4 Lawsuits are also sure to ensue.

Although this presents a substantial risk to the municipal market, we are hopeful the resurrection of the 28% cap would apply to new issues only to avoid disruption to the market. However, more education is needed, as each new iteration of the attacks on the exemption seems to come with only a blurry understanding, at best, of the potential impacts to investors and issuers. In the meantime, we believe some compensation to reflect the risk of a policy misstep is warranted, and see the recent selloff as a fair representation of investor fears and probabilities of a worst case outcome.

1 Does anyone remember bearer bonds?

2 There is also a pull forward effect happening now where many issuers are loading issuance into 2025 before any potential policy changes take effect. There has been a notable increase in issuance in higher education, for example, where threats to the exemption are greater.

3 We won’t bore you with the math here. Contact us for an explanation, if interested.

4 We can equate this to issuers’ perception of subsidies under the Build America Bond (BAB) program. After subsidies were first cut by sequestration in 2013, issuers lost all faith in the federal government to deliver on its promises through this structure. When subsidies have come up as a potential alternative to the tax-exemption in subsequent Congressional discussions, they have fallen on deaf ears as issuers have no appetite to take on that risk again. To make matters worse, BAB subsidies were also included on the menu of pay-fors in the leaked House Committee report from January, which likely led to at least one additional exercise of a BAB ERP this year, despite less favorable refunding economics than in 2024.